So changing some numbers can lead to big tax increases.

getty

There are some significant tax increases being proposed by the Biden administration (and also by Congress). It’s incredible how changing a number or two dramatically increases taxes, and also changes policies, which start a chain reaction of cascading results. Buyer attention: Make your own conclusions about whether tax increases are good or bad. This discussion focuses only on possible outcomes.

Change an ‘8’ to a ‘1’ and raise over $ 1 trillion. Part of the tax proposal is to increase corporate tax on C-corporations from 21% to 28%. At first glance, this seems and it will hit big companies. Estimates vary, but a tax increase to 28% will negatively impact the bottom line of the S&P 500, possibly by as much as -6%. Lower earnings mean investors pay less for a stock.

Large, profitable companies pay more taxes, but there are only about 3,671 publicly traded companies (in 2020) versus about 23 million private companies. According to Ashley Wilson, chief tax lobbyist for the US Chamber of Commerce, “the corporate rate increase will cascade for almost all small businesses as well.” Part of the reason is the particular way businesses are taxed. A company is a separate legal entity and pays taxes as a taxpayer. This is the typical type of company known as a C company and named after the associated sub-chapter of the Internal Revenue Code. There are approximately 1.4 million small businesses (under 500 employees) that are C-Corps. However, the vast majority (about 95%) of American businesses are transit companies. Pass-through means that the profits and losses go into the owner’s tax return. Pass-through businesses include sole proprietorships, limited liability companies (LLCs), and sub-chapter S companies (also named after a sub-chapter of the Internal Revenue Code). Take a quick poll on a drive and count how many Small Businesses (LLC, PLLC, Inc.) you see. Most of them are passages and virtually all of them would likely be affected by a tax hike.

The tax code has to put both types of business on par, and that is the problem. If we tax C-Corps at 28%, we must allow pass-through owners to deduct 20% of their business income (known as Qualified Business Income or QBI). Otherwise the C-Corps would have a lower tax rate. If we increase the company rate, lawmakers would have to change the rules of passage and lower the deduction. Hence, increasing the business rate affects most small businesses.

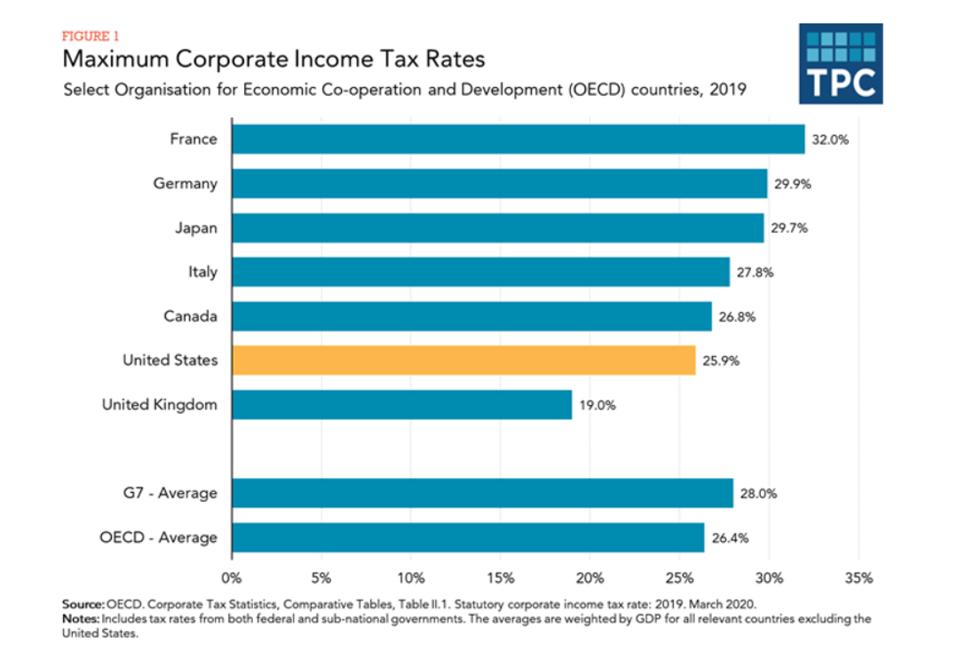

The third level effect concerns competition. Of the G7 industrial nations, the US has the second lowest corporate tax rate.

Here is a comparison of the maximum corporate tax rates in G7 countries.

OECD, corporate tax statistics, comparison tables

If corporate rates rise to 28%, the US will move up two places to fourth, at the level of the current G7 average and above the G20 average (26.4%).

Change a ‘5’ to a ‘1’ and Upend Estate Planning. Of all the possible tax hikes, the easiest (and probably the most obvious) thing to do would be to change the expiration date of the Tax Cut and Jobs Act (TCJA). The TCJA has several provisions that will expire on December 31, 2025 due to the voting process. Two notable items in the D-Pad are the maximum ordinary income tax rate from 37% to 39.6% and the estate tax exclusion decrease from $ 11.7 million to $ 5.85 million. If you change the expiration date to 12/31/21 you will increase taxes for high income, high net worth families. The income tax hike is substantial, but not particularly momentous. The 37% tax rate starts at $ 523,601 for a single person and $ 628,301 for a married couple, hitting a more dilute group of taxpayers.

The inheritance tax change is binary. If you taxed $ 5.85 million at 40% (45% suggested), the deceased’s family would be hooked for about $ 2.34 million. Married couples are each given an exclusion so they can move on to $ 23.4 million now and $ 11.7 million when it expires. The problem arises for couples worth more than $ 11.7 million or for individuals worth more than $ 5.85 million. Their heirs pay more taxes. $ 5.8 million sounds like a lot, and depending on your point of view, it is. However, a single person in California may have a $ 1.2 million home (your basic CA starter home), a 401 (k), or a $ 1 million IRA, $ 1 million investment. USD and life insurance of USD 1 million. They have roughly $ 4.2 million, but if their wealth grows a modest 5% they would be worth $ 9.2 million in 20 years and part of the estate would be taxable. There’s also the little thing about California death taxes. Estate planning lawyers and advisors are seeing a huge rush of planning steps ahead of the move. Wayne Roberts, Co-Chief Tax Counsel of the Bodman Law Firm in Michigan, notes, “Reducing the foreclosure will create many more taxable estates, and increasing the tax rate to 45% will exacerbate the economic impact for those who are not involved in the business strategic planning early. Customers would be well advised to monitor legislative action regularly and begin revising their estate plans now. Even a slight delay could have a significant negative impact. “

Bottom line. Simple changes in tax law can have huge consequences. We do not know which tax increases may actually come into effect. We should note that the US took on billions in debt during the pandemic. Someone always pays for it, and the easiest way for the government to increase revenue is through taxes. The correlation is hard to ignore.

As always, I’ll try to answer questions by emailing [email protected].