Iowa property taxpayers are getting more and more frustrated and tired of blaming local governments for not answering why tax breaks are next to impossible. Property taxes fund local governments and often the debt is shifted from one tax agency to another to justify why the tax bills are high. In addition, local governments are also reacting to the fact that lowering property taxes will lead to cuts in key services such as the police, fire and emergency services.

Iowa property taxpayers deserve a solution, and luckily there is a solution that will make local governments more transparent and accountable. Introducing a tough tax truth-finding law will provide the solution property taxpayers are looking for and will force local governments to be more accountable to taxpayers.

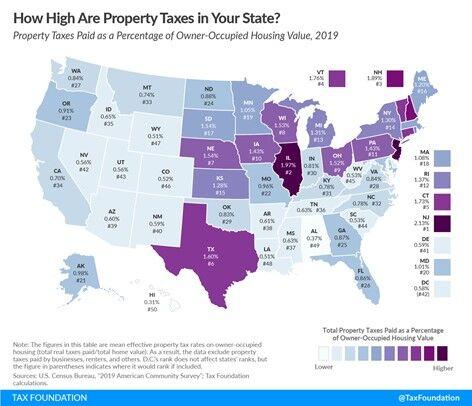

Since 2000, Iowa property taxes have risen 122 percent faster than population, inflation, and the cost of living adjustment for social security. The tax foundation ranked Iowa has the nation’s 10th highest property tax rate.

Local government spending is at the heart of high property taxes. Too often the district assessor is blamed, but taxpayers need to focus their attention on the expenses. Whether wealth tax or income tax, spending leads to high taxes. Additionally, many Iowa property taxpayers often wonder why they are told their taxes have been lowered but their property tax bills are higher.

This is because many local governments can easily hide behind elevated ratings and collect the windfall while the appraiser takes the blame. This has led to an “honesty loophole” in property taxes. Without taking into account local government spending, it will be difficult to implement tax relief on land transfer tax. The wealth tax is also a form of wealth tax. For example, if the value of a home has increased by 10 percent, that doesn’t mean the homeowner has increased their savings by 10 percent to cover their property tax.

In 2019, Iowa legislature passed a property tax accountability and transparency measure. This new law requires Local governments such as counties and cities (school districts not included) hold a public hearing if the proposed budget is increased by more than 2 percent year-on-year, and a majority majority in favor. This new “soft upper limit” of 2 percent is intended to control the growth in property taxes and requires local governments to be more transparent in the local budget process.

The law has been labeled a “truth-in-taxation” measure, but has failed in strength when compared to similar laws. The 2019 law needs to be strengthened by obeying the Utah Truth-Finding Act. Utah’s law is considered the gold standard for property tax reform and is the most taxpayer-friendly property tax law in the country. Since 1985, Utah’s Tax Truth-Finding Act has provided property tax relief by slowing property tax growth. The Tax Foundation ranks Utah with the seventh lowest real estate tax rate in the country.

Source: Tax Foundation (Note: Iowa ranks 10th highest in the nation)

Utah’s Tax Truth-Finding Act is an income-based restriction, which means that as valuations go up, property tax rates go down. The Truth-in-Taxation Act guarantees that every taxpayer receives the same property tax income as in the previous year, including new income. This prevents local governments from getting a godsend because ratings have gone up. “Local governments shouldn’t automatically get a 12 percent increase in income just because property valuations are up 12 percent,” wrote Howard Stephenson, who recently retired as president of the Utah Taxpayers Association and is a former state senator.

If a local government wants to exceed the certified tax rate, it requires a truth-finding hearing, which is accompanied by an extensive public notification and consultation process. Truth-in-taxation also forces local government officials to cast recorded votes to approve an increase in tax revenue.

Through the truth-finding process, local governments need to justify why they want to raise taxes on additional expenses and force them to be more transparent about why they need additional tax revenues. A key aspect of Utah law is a direct notification requirement, sending notices to taxpayers containing information about the proposed tax increase and its impact on their tax bill. It also includes the date, time and place of the household hearing to determine the truth in tax law. This extensive public notification and consultation process has been successful and Utah taxpayers are actively participating in tax truth-finding hearings.

Rusty Cannon, president of the Utah Taxpayers Association, argues that Utah’s law provides “sunlight” over the local government’s budgeting process. Cannon noted that while “decisions to increase taxes can be made, the law only requires that they be done in sunlight – that essentially you have to argue to voters and taxpayers why the increase in revenue is necessary”.

The truth about taxation is accountable and makes tax authorities think twice about tax increases. “You do it in a public setting, you tell them how much your liability increase will be, on a package basis, so everyone has this full disclosure. So there is no such thing as automatic inflation creeping in. There is no automatic increase. There is no automatic stroke of luck when real estate values rise. It keeps property taxes under control. However, if they want to raise them, they just have to do it in this public process, ”Cannon said.

Jonathan Williams, chief economist for the American Legislative Exchange Council, described the success of Utah’s truth-finding law on taxation:

Utah’s Truth In Taxation Act has effectively controlled the growth of its property tax bills and aggregate charges. The law requires citizens to be informed of the intention to raise taxes and to be invited to a public hearing to raise concerns. This also allows local government agencies to make their case if they feel that additional revenue may be required. If a local government decides to increase spending, the truth-finding process requires that elected local officials cast recorded votes to approve the new rates or ratings.

Recently, Kansas and Nebraska passed property tax reform laws based on Utah’s Truth-in-Taxation. Kansas law serves as the closest example of Utah law because of its strength. Dave Trabert, president of the Kansas Policy Institute, argues that the new Kansas law “closes the honesty gap in property taxes.” “Local officials can no longer pretend to” hold the line “on property taxes while accepting large increases from valuation changes. Now they have to be honest about the whole tax hike, ”said Trabert.

Specifically, the Kansas Act lifts the property tax cap, which is largely ineffective due to the numerous exceptions, and from 2021 the mill rates will be reduced so that revaluations bring in the same amount of property tax. If a tax authority wants to increase the property tax, it has to hold a public hearing and vote on the possible increase. This also includes a direct reporting process that must include:

- The revenue neutral rate for each relevant tax break;

- The proposed tax rate and the amount of tax revenue that should be collected by each taxing subdivision in order to exceed its revenue neutral rate;

- The tax rate and amount of each tax subdivision for the property from the previous year’s tax return;

- The estimated and fixed value of the taxpayer’s assets for the current year;

- The estimated tax amount for the current year for each subdivision based on the neutral rate and any tax rates in excess of the neutral rate and the difference between those amounts for each taxable subdivision that wishes to exceed its neutral income rate;

- The date, time and place of the public hearing for any tax subdivision attempting to exceed its revenue neutral rate; and

- Information on the State of Kansas State Mill Duty.

The Kansas Truth-Finding Act already works for taxpayers. Several cities and counties are not going to increase their property taxes next year, while others are considering small increases.

Iowa policymakers should seriously consider following the example of Utah and Kansas in adopting a tax compliance measure that requires strict direct reporting. Taxpayers deserve to know how much their property taxes will rise, and Utah and Kansas are demonstrating that truth-finding laws enforce more “sunlight” and accountability for the budget process on local governments.

Officials shouldn’t be afraid of establishing the truth. Greater accountability and transparency will only improve local government. “Just like someone who doesn’t want to be seen in a bathing suit should avoid the beach, those who don’t want to make decisions in public shouldn’t run for public office,” Cannon said, referring to government transparency.

“And the idea behind Truth in Taxation is that you can make the choice, you just have to be open about it,” noted Cannon. In addition, elected officials should explain to taxpayers why they need additional expenses. Too often, governments at all levels forget that the money is part of the taxpayer’s hard work.

In the past few years, Governor Kim Reynolds and lawmakers have made significant strides in lowering Iowa’s high tax rates. Much remains to be done to reduce individual and corporate income taxes to make the Iowa economy more competitive. The same applies to property tax. High property taxes hold back economic growth and provide an incentive for people to either leave Iowa or not to settle in Iowa.

It is time to implement a proven solution to provide tax breaks for Iowa taxpayers. Other reforms like freezing property taxes for certain taxpayers or investment restrictions may sound promising, but these “solutions” will not solve the problem. The goal should be wealth tax relief for all powerers, and truth-finding will benefit all taxpayers.